Contents

Scroll to:

https://doi.org/10.17747/2618-947X-2019-4-320-329

Scroll to:

Transition to digital technologies in management of power industry at all levels – an inevitable consequence of the technical progress which has generated opportunities for diversification, decarbonization and decentralization. Thus it is necessary to recognize that digitalization in power industry is NOT automation, and first of all creation of new business models, services and the markets with a support on possibility of digital economy. In this article questions of transformation of architecture of power industry, and also the main restrictions are considered: absence in regulatory base of new opportunities for consumers; general system inefficiency; impossibility “to legalize” appearance of new subjects (active consumers and prosumers, operators of micropower supply systems and aggregators of the distributed power objects, various service organizations), and also to deregulate the relations between them, to standardize interaction interfaces with EEC, to transform the energy markets.

In article it is offered for transition to new digital power to make corresponding changes to the legislation: to enter new type of participants of the market (the active consumer, an active power complex), operated intellectual connection carrying out the standard with the electrical power system, completely responsible for management of the power supply and thus having the minimum regulatory restrictions on organizational model of the work; to improve rules of functioning of trade systems for creation of the markets of the distributed power providing an effective exchange of goods and services between traditional participants of the markets and participants of new type; to enter possibility of application of technologies of the coordinated management of the distributed sources and consumers of energy, systems of storage of energy, means of regulation of loading (“aggregators”) for the purpose of increase of efficiency of their use and participation in the electric power and power markets, including rendering system services and performance of other functions in these markets (the pilot project of such system is realized under the leadership of the author of the present article by subsidiary PAO “Lukoil” “Energy and gas of Romania”); to increase technological and economic flexibility of conditions on reliability and quality of power supply, creation of possibility of a choice by the consumer of conditions of power supply necessary for him and the account them in cost; to enter the accounting of the opportunities given by “new” decisions, at an assessment, formation and implementation of investment programs of the adjustable companies (including introduction of a technique of an assessment of investment projects at possession cost on all life cycle of the decision); to replace cross subsidizing of the population by industrial consumers with mechanisms of address social support and / or with system of restriction of volumes of consumption on reduced rates (“соцнорма”); to refuse further deployment of system of subsidizing of power supply of one regions at the expense of consumers of other regions (as it leads to growth of inefficient power consumption in the subsidized regions, not provided with available generation and infrastructure); to change norms of technical regulation, norms of design on the basis of new technologies; to make changes to programs of development of the infrastructure organizations of power industry taking into account trends of diversification, decentralization, decarbonization and a digitalization; to provide possibility of stimulation, including tariff, implementation of regional programs (pilot and regular), aimed at the complex development of power industry on the basis of new approaches, technologies and the practician, and also the hi-tech companies of small and medium business providing development.

Zubakin V.A. STATE STIMULATION OF TRANSFORMATION OF POWER INDUSTRY. Strategic decisions and risk management. 2019;10(4):320-329. https://doi.org/10.17747/2618-947X-2019-4-320-329

It is customary to describe the transformation of the world’s power industry to be “standing on four whales”, or, otherwise, on 4D: diversification, decarbonization, decentralization, and digitalization. Let’s consider the reasons and consequences of these processes, the economic signals received by business in Russia and abroad, particularly, under the influence of scientific and technological progress and by virtue of state regulation, and finally, the changes in management systems at micro- and macro-levels that are generating these processes.

It should be noted at once that we don’t consider the notorious “depletion of energy resources” to be the reason for transformation of global power industry. As George Simon has proved, any limitation of natural resources is solved with the aid of scientific and technical progress: for example, from former importer of agricultural products, Israel has turned into exporter after introduction of drip irrigation; the USA became the global leader in hydrocarbon output due to “shale revolution”; in Western Siberia, on sites of traditional oil extraction with already depleted fields, there is the socalled Bazhenov Formation with a reserve of 2.5 billion tons of oil [Renewable energy statistics…, 2018]. And there are many similar examples.

What transformations of power industry take place in each of these D-directions?

1. Diversification at macro-level reveals itself in the structure of the country’s energy balance, when the part of “non-fuel” power generation, such as renewable energy sources and nuclear power, is growing rapidly beside the traditional sources of energy (hydrocarbons). Moreover, it has already reached over 20% of overall consumption of all types of energy in developed countries, with a tendency towards further growth.

For countries with insufficient energy supply (of hydrocarbons), diversification of that kind simultaneously increases their level of sustainability and development security. Energy diversification at micro-level reveals itself in many forms. For example, there is a rapidly growing stock of electric cars, natural gas and fuel cell vehicles and various hybrids in automotive sector. The automation of combustion management brought about the emergence of multi-fuel power plants in electric power and heat power industry, which could be used with solid, liquid and gaseous fuels including various industrial and household wastes; moreover, the speed of shift from one type of fuel to another is measured in minutes now. In addition, there are new effective technologies for transition of different types of fuels into each other (solid – into gaseous and liquid, liquid – into solid and gaseous, gaseous – into liquid).

2. Decarbonization – an increase of the energy output and consumption without the use of hydrocarbon fossil fuel is a stable tendency either in developed and developing countries, though for different reasons.

The countries of Europe and Northern America, as well as Japan, have a strong public opinion about the need to struggle against global warming. Other countries are prompted to decarbonization by ecological problems: predominance of coal power generation, cities overloaded with environmentally harmful vehicles, rapid industrial growth on the basis of backward technologies1.

All of it forces the governments of developing countries to take decarbonization seriously, in spite of a very pragmatic attitude to the problem of global warming. A tenfold reduction in the unit cost of equipment for renewable energy over the past 30 years has made these sources of energy competitive with traditional ones and quite affordable for the poorest countries2.

3. Decentralization – a shift in the grid architecture from hierarchical principle of its construction to a network principle. Some researchers [Rol' mikrogeneratsii …, 2017] even talk about cellular power industry.

Technical progress and creation of compact efficient lowpower energy sources (microturbines, photovoltaic modules, fuel units) broke the traditional functional correlation “the larger, the more efficient”; the effect of scale in power industry was defeated by the opportunity to bring a source of power closer to a consumer and save on transmission, also to increase its reliability.

Moreover, the modern efficient energy storage systems made self-balancing possible for consumers with their own energy sources, having transferred this function from the public grid to their own microgrid in scale of their household, enterprise or settlement.

The growth rate of the total distributed generation capacity is steadily surpassing the growth rate of traditional generation capacity supplying power grids of common use, and in a vast majority of countries around the world at that [Linder, Lisovskiy, 2017].

4. Digitalization is a shift to the power industry with the widespread use of digital control devices connected to the Internet information networks at all levels of a power system from generator devices and power grids to an end, including domestic, consumers of electricity that provides the possibility of intelligent grid management based on machine-to-machine (M2M, IoT) interaction.

The point is that a large-scale transition to environmentally harmless carbon-free energy industry leads to decrease in its systemic efficiency: stochastic generators using solar and wind energy require creation of the reserve generating and/or storage capacity. We consider that the basic solution for the problem of growing energy industry inefficiency is a shift to the decentralized organization of capacities, management and energy markets, that provides an effective combination of large and small distributed generation and a better satisfaction of differentiated and dynamically changing customer requirements.

But the joint operation of a huge number of distributed subjects in conditions of decentralizing architecture has one principal problem – the complexity of their management is increasing along with the rising number of interacting participants. Digitalization is a technological basis, which makes it possible to resolve this problem.

Traditional centralized architecture of power industry has significantly exhausted its efficiency potential and, in conditions of the 4-D transformation, can’t be considered as more effective and optimal. New challenges of the 21st century are:

Let’s consider the effect of these challenges on the power industry management system at macro- and micro-levels.

The issue of stability and predictability of rates and prices on energy carriers is one of the most important for an investor, who plans to implement a construction project of power-consuming production. If the rates and prices on the energy carriers grow faster than a consumer is able to raise the price on his product, the hedging against this risk will be needed, particularly, by way of creation of his own source of electrical and/or thermal energy. Preventing crosssubsidization, the size of which is constantly growing in the Russian power industry, creates an additional effect for the investor [Trachuk, Linder, 2017b].

A consumer, who creates his own energy park, reduces the revenue base of generating and grid energy companies, a regulator is forced to raise the rate, and creation of one’s own energy park becomes beneficial for wider range of consumers. The revenue base is reduced again, the rates are raised again, and economic signals for consumers to invest into the energy self-supply appear once more. This kind of “positive feedback system” inflicted the most severe damage to the centralized heat network and cogeneration in Russia [Linder, Trachuk, 2017]; and now, if the management system for development of power industry will not be changed, the sphere of electric power generation might be the next.

The energy equipment for consumers - both industrial and domestic - is constantly becoming more complicated and increasingly demanding on the quality and reliability of energy supply. A one-minute interruption in operation of a modern oil refining enterprise leads to disruption of the most complicated process chains and subsequent return back to normal operation mode during the next several days with multi-million economic losses. A failure in energy supply of the data center leads to disruption of many financial transactions, loss of information and steep losses. A failure in energy supply of infrastructure facilities (transport and communication) poses a threat not only for business, but for many human lives. The increasing complexity of technologies in all spheres of economy and society has made them fragile and dependant on the quality of energy supply.

Consumers have formed a demand for the energy selfsupply equipment, and business has provided an adequate supply of everything needed for it. The most striking example is the TESLA Powerwall2 for energy supply of a building for the whole day. It is easily installed (plugand-play principle) both indoors and outdoors, has an in-built inventor for the energy conversion from solar photoelectrical panels into alternating current [Sharovarov, 2015]. There are solutions for industrial enterprises of any amount and structure of consumption in the market. The affordability barrier for consumers is overcome with the aid of various financial schemes (leasing or energy performance contract).

Today’s consumers are “spoiled” by many new modern business schemes and services in transport, communication, trade, and don’t understand, why the readings of the electricity meter in their apartment should be taken by themselves and why they should spend long time listening to the mantra about importance of a call from every client in the call-center queue to submit his or her meter readings.

The efforts of the Government of the Russian Federation to simplify and accelerate technical connection to power grids are undoubted; however, this problem is not solved in the most interesting, for business, cities and regions.

It should be recognized, that the enumerated challenges and problems are characteristic feature of all countries, not only of Russia. The centralized architecture implemented in existing power grids of the countries around the world is not able to respond effectively on the mentioned challenges with its unidirectional power flow from large power generation to distributed consumers, united hierarchical electricity market and dispatch control, the roles in a power system and the quality levels of energy supply that are unified to the level of standards.

Only distributed power industry with decentralized management and markets, as well as wide engagement of all users of power grids into the process of managing them, can satisfy the requirements. Distributed generation, energy storage systems and adjustable load of end users integrated with each other and with the centralized power system, are the still unused resource for increase in efficiency of power grids. Distributed power industry raises the power grid efficiency on account of reducing the need in the connected capacity, new local self-balancing associations of low-power generators and users, also engagement of the end users’ energy assets into the processes of managing the power grid, which makes it flexible. But, in the existing architecture, the large-scale development of distributed power industry faces with the rise of various costs:

There is one principal problem – the complexity of management is increasing along with a number of interacting participants. Since a consumer becomes an active participant in the process, the management becomes multiagent, when every participant of a collective transaction has the right of vote in decision making and contributes to the final result – either generation of power or, inversely, unloading, i.e. “negative power” supply. Digitalization is a technological basis, which makes it possible to resolve the problem.

A shift to digital technologies in management at all levels of power industry is an inevitable result of the technical progress, which brought about the possibilities for diversification, decarbonization and decentralization. At the same time it is necessary to proceed from the fact that digitalization in power industry is NOT automation, but first of all, creation of new business models, services and markets with reliance on possibilities of digital economy. A simple example from the other branch: creation of automated system for dispatch control of a taxi depot is automation, but Uber, which represents the new business model of the same service, which at the same time is not a taxi depot and has no cars, but makes it cheaper and more comfortable – that’s digitalization.

In digital power industry, it is important to determine the new business model, the potential of which is unlocked through penetrating communications, machine-to-machine interactions and digital modeling. Many such business models have already been developed in the world: demand aggregators, virtual power plants, virtual distributed energy storage, energy hedging, etc.

These costs should be minimized in the new architecture of distributed power industry, and the distributed power industry itself should increase the operational efficiency of the power grids as a whole. Power grid, constructed according to the new architecture [Khokhlov, 2017; 2018; Fardiev, 2018] should become:

A user of such system is integrated in it through interfaces and becomes a full-fledged participant of new services and business models.

According to this view the energy internet is an ecosystem of technically and economically interconnected users. Structural and technological peculiarities of the grid construction will resemble the Internet, so the new approach is often called the Internet of Energy. The owners of any electric power equipment (industrial, commercial, domestic), which is able to generate, store and consume electrical energy, as well as subjects providing various services for the owners of electric power equipment, can be users of the Internet of Energy.

Pools of equipment, which have a common point of connection to the power grids and information channels ensuring communication with the Internet of Energy, form its structural unit – an energy cell, which interacts with other energy cells as a unified whole regardless of composition and complexity of its internal structure [Tsifrovye tekhnologii…, 2017].

The users of the Energy Internet, with the aid of their energy cells, can play various dynamically changing roles in the power system, providing services to each other, such as supply of electricity, participation in operation mode control, including maintenance of voltage frequency and level, provision of energy equipment for virtual rent, provision of power reserve and any other services that could be provided in power industry.

Interaction of cells is energy transactions forming the multiagent decentralized economic and technological management of a power system.

Energy transaction is an act of technical and economic interaction between users and relevant energy cells, in which operation parameters of the energy cells are coordinated, so one party of energy transaction acquires some useful quality, value, and the other receives payment for this value.

For the purpose of robotized provision and obtain of these services the users turn to applications of the Internet of Energy. Applications are the service programs that independently build the interaction between the energy cells by virtue of forming the sets of energy transactions for realization of certain services. Coordinated operation of the energy cells due to balanced market relationships between the users gives the characteristic feature of an ecosystem to the internet of distributed energy industry.

The architecture of the Internet of Energy should provide, on the one hand, a possibility to implement energy transactions, on the other hand – a possibility to manage the energy cells through machine-to-machine interaction, and finally, a possibility of such distributed operation mode control in real time that makes it possible to maintain the power balance in the power system, as well as its static and dynamic sustainability.

The Internet of distributed energy industry is a system of systems (SoS), the architecture of which is built based on a special combination of three systems [Trachuk et al., 2018]:

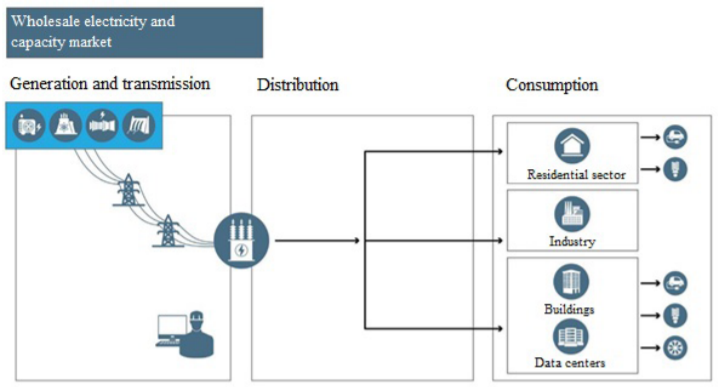

The modern technical architecture of the Russian power industry was developed as a whole by the middle of the 20th century; it has not undergone qualitative changes since then and is built largely on the principles and technologies of those years (fig. 1) [Trachuk, 2011]. Restructurization (division on competitive and monopolized types of activities) and liberalization (wholesale energy and capacity markets) changed nothing in technology of generation, though observability and measurability in the power industry has significantly increased: a system operator sees the generating equipment in real time, all limits for the wholesale market subjects are covered by automated information-measuring system of power consumption (AIISKUE) [Trachuk, 2010а; 2010b].

Despite the market transformations and certain upgrade of information systems, the developed architecture of the power industry in Russia is built, as before, on principles of enlargement of capacities, centralization and hierarchy. This architecture need to be significantly changed to be able to respond adequately on challenges of diversification, decarbonization and decentralization of the power industry.

We agree with the authors of the study [Dyadkin et al., 2018] that the indicators of the energy transition for Russia may be:

The main principles of the new architecture (Fig. 2) [Knyaginin, Kholkin, 2017] will be:

The issue of power industry transformation came to Russia from outside. At the value level in society, as well as at the level of the public policy, the relevance of the main message for the transition – decarbonization – is not of “alarmist degree”.

Russia has joined the Paris3 Agreement. Russia’s contribution to the Paris Agreement will be the limitation of greenhouse gas emissions to 70 % of the base level of 1990 by 2030.

This means that Russia will keep emissions at the same level for 30 years, significantly offsetting the increasing emissions in other countries and regions around the world. It is planned to achieve this objective by way of introduction of new energy-saving technologies, increasing energy efficiency of the economy, development of renewable sources of energy, and all this is impossible without qualitative transformation of the electric power sector4.

Peculiarities of power industry organization in Russia: long-distance infrastructure, low density of electricity consumption, large share of industrial load, socially oriented policy, imperfection of the market and regulation of the sector – lead to a constant increase in prices on electricity for business and gradually become a constraining factor for economic development of the country [Trachuk, 2011а, 2011b].

The inertial scenario for the sector development in the near future will lead to a situation, when the price on electricity for the industry in Russia will exceed the price in the USA and will be almost equal to the average price in the EU countries. This will negatively affect the compatibility of exported products of the Russian industry with its traditionally high energy intensity [Snizhenie energoemkosti VVP, 2016].

It should be noted that world’s leading energy companies try to respond adequately on the transformation challenges described in the 4D formula. In 2016, the E.ON group has segregated the thermal power stations and international trade of energy sources into a separate company Uniper, having focused on renewable energy industry, power grid business and new customer services – distributed generation, energy efficiency and energy storage technologies [World Energy Outlook, 2017a].

In the same year, the company EDF adopted the CAP2030 strategy, the key aspects of which were proximity to consumers (assistance in managing the energy consumption through smart digital technologies), doubling of renewable energy capacities with life extension of existing nuclear power plants, intensified activities in the international markets of carbon-free generation, consumer services and engineering [Vorobyova, 2016].

In 2016, Enel announced the OpenPower strategy, which includes, among other things, disclosure of new energy technologies (in particular, renewable energy sources and smart grids), new ways for management of the energy efficiency (through smart metering, digitalization), as well as a new way for the use of electrical energy, first of all in electric vehicles, for the world.

Similar changes occur in related industries, such as machine industry and engineering. Thus, in November of 2017, Siemens announced the intension to reduce the jobs in production of large turbines, the demand for which is falling with the growth of decentralization and markets of solar and wind energy, up to seven thousands of workers [Trachuk et al., 2018].

The Government of the Russian Federation and the energy companies are actively thinking about the energy transformation. In 2017, the Digital Economy Program of the Russian Federation was developed and approved, the formation of sectorial programs for digital transition, in the power industry as well, began. On May 7, 2018, the President of the Russian Federation V.V. Putin signed the decree “On National Goals and Strategic Tasks of the Development of the Russian Federation for the Period until 2024”, which determined the priorities for digital transformation of the country’s economy, including the power industry sectors. In the professional community of power engineers, there is an understanding that the existing technological structure in the power industry has reached the limit of its efficiency and, in a five year perspective, will be less competitive in a number of spheres, where consumers have higher requirements for reliability, quality, accessibility and environmental friendliness of the energy supply, compared to solutions of the new – digital – power industry. Major changes will affect the “last mile”, which is based on the infrastructure of distribution grids of 110 kW voltage and lower. Thus, in the Russian energy policy, it is proposed to carry out a maneuver for development of a retail segment of the power industry on principles of the Internet of Things.

Taking into account that the majority of distribution grids are owned by the state holding company PAO “Rosseti”, it is necessary to form the public position to respond adequately on challenges of the power industry transformation.

To implement the energy transition and significantly rebuild its architecture, it is necessary to carry out largescale amendments to its legal and regulatory framework.

Legal regulation of the market after amendments must ensure the formation of regulatory conditions for development of the power industry in this direction. The main limitations are that the new regulatory base must:

The main obstacle to this reform is that the market participants and infrastructure organizations are not interested in transition to the new architecture in the current institutional environment, and retail consumers and subjects of distributed power industry remain beyond the field of competitive mechanisms and face the regulatory barriers for realization of new approaches to the energy supply: liberalization degrees of the wholesale and retail markets of electricity are drastically different.

In addition to this key obstacle, it is worth to highlight:

The increase in cross-subsidization is also noteworthy: as it was revealed in studies, one of which had been carried out with participation of the author of this article [Linder, Trachuk, 2017; Trachuk, Linder, 2017b; Trachuk et al., 2018], despite the declared principles of the need to remove it, its actual amount keeps growing, distorting the economic signals for participants of the energy markets.

The most practicable way in Russia is to determine a well-balanced model of the power system, which will ensure optimal combination of elements of the new power industry and the centralized, traditional one [World Energy Outlook, 2017b].

To do it, it is necessary to do relevant amendments to legislation concerning the power industry:

1. The 2016 ACEEE international energy efficiency scorecard. URL: http://www.efficienzaenergetica.enea.it/allegati/Report_ACEEE%202018.pdf/ (accessed on 25.10.2019).

2. The internet of energy: Architectures, cyber security, and applications (Part II) // IEEE.org. URL: http://ieeeaccess.ieee.org/special-sections-closed/internet-energy-architecturescyber-security-applications-part-ii/ (accessed on 27.10.2019).

3. Government’s report on the state of energy conservation and energy efficiency in the Russian Federation in 2016. URL: https://minenergo.gov.ru/system/download-pdf/5197/76456 (accessed on 06.10.2019).

4. Government program “Energy Savings and Energy Efficiency Improvement for the period till 2020”. URL: https://minenergo.gov.ru/node/441 (accessed on 17.10.2019).

1. Vorobeva Yu. (2016). Solntse, veter i voda: Portugaliya proderzhalas̕ 107 chasov na “zelenoy” energii. Vesti.RU. May 30. URL: https://www.vesti.ru/doc.html?id=2759535&tid=107662 (date of access: 27.10.2019).

2. Dyadkin D., Usoltsev Yu., Usoltseva N. (2018). Smart-kontrakty v Rossii; perspektivy zakonodatel̕nogo regulirovaniya. Universum: ekonomika i yurisprudentsiya, 11 (date of access: 27.10.2019).

3. Knyaginin V. N., Kholkin D. V. (2017). Tsifrovoy perekhod v elektroenergetike Rossii. Ekspertno-analiticheskiy doklad. URL: https://www.csr.ru / uploads / 2017 / 09 / Doklad_energetika-Web.pdf (date of access: 10.10.2019).

4. Linder N. V., Lisovskiy A. L. (2017). Razvitie rynka elektroenergii v Rossii: osnovnye tendentsii i perspektivy. Strategii biznesa, 2, 48–54.

5. Linder N. V., Trachuk A. V. (2017). Vliyanie perekrestnogo subsidirovaniya v elektro- i teploenergetike na izmenenie povedeniya uchastnikov optovogo i roznichnogo rynkov elektro- i teploenergii. Effektivnoe antikrizisnoe upravlenie, 2, 97.

6. Raspredelennaya energetika v Rossii: potentsial razvitiya (2018). Moscow, MShU Skolkovo.

7. Rol’ mikrogeneratsii na osnove VIE v razvitii raspredelennoy energetiki Rossii (2017). Moscow, MShU Skolkovo. URL: https://events.vedomosti.ru / media / materials / materials_0–41324120353862437 / download (date of access: 17.10.2019).

8. Sistemy upravleniya energetikoy budushchego (Internet of Energy). URL: https://energy.skolkovo.ru / ru / senec / research / internet-of-energy / (date of access: 11.10.2019).

9. Snizhenie energoemkosti VVP (2016). Minenergo Rossii. URL: https://minenergo.gov.ru / node / 441 (date of access: 27.10.2019).

10. Trachuk A., Linder N., Zubakin V., Zolotova I., Volodin Yu. (2017). Perekrestnoe subsidirovanie v elektroenergetike; problemy i puti resheniya. Saint Petersburg, Real’naya ekonomika.

11. Trachuk A. V. (2010a). Otsenka sostoyaniya konkurentnoy sredy na optovom rynke elektroenergii. Ekonomicheskie nauki, 66, 124–130.

12. Trachuk A. V. (2010b). Riski rosta kontsentratsii na rynke elektroenergii. Energorynok, 3, 28–32.

13. Trachuk A. V. (2011a). Razvitie mekhanizmov regulirovaniya elektroenergetiki v usloviyakh ee reformirovaniya. Ekonomika i upravlenie, 2 (64), 60–63.

14. Trachuk A. V. (2011b). Reformirovanie estestvennykh monopoliy: tseli, rezul’taty i napravleniya razvitiya (monografiya). Moscow, Ekonomika.

15. Trachuk A. V., Linder N. V. (2017a). Innovatsii i proizvoditel’nost’: empiricheskoe issledovanie faktorov, prepyatstvuyushchikh rostu metodom prodol’nogo analiza. Upravlencheskie nauki, 7 (3), 43–58.

16. Trachuk A. V., Linder N. V. (2017b). Perekrestnoe subsidirovanie v elektroenergetike: podkhody k modelirovaniyu snizheniya ego ob’’emov. Effektivnoe antikrizisnoe upravlenie, 1 (100), 24–35.

17. Trachuk A. V., Linder N. V., Tarasov I. V., Nalbandyan G. G., Khovalova T. V., Kondratyuk T. V., Popov N. A. (2018). Transformatsiya promyshlennosti v usloviyakh chetvertoy promyshlennoy revolyutsii. Moscow, Real’naya ekonomika.

18. Fardiev I. (2018). Novaya epokha v energetike. Respublika Tatarstan. April 25. URL: http://rt-online.ru / novaya-epoha-v-energetike / (date of access: 27.10.2019).

19. Khokhlov A. (2017). Vozobnovlyaemye istochniki energii: novaya revolyutsiya ili ocherednoy puzyr’. Forbes.ru. May 2.URL: http://www.forbes.ru / biznes / 343591‑vozobnovlyaemye-istochniki-energii-novaya-revolyuciya-ili-ocherednoy-puzyr (date of access: 11.10.2019).

20. Khokhlov A. (2018). Raspredelennaya energetika v Rossii: potentsial razvitiya. Moscow, MShU Skolkovo.URL: https://energy.skolkovo.ru / downloads / documents / SEneC / Research / SKOLKOVO_EneC_DER-3.0_2018.02.01.pdf (date of access: 11.10.2019).

21. Tsifrovye tekhnologii v setevom komplekse (2017). Energeticheskiy byulleten’. October. URL: http://ac.gov.ru / files / publication / a / 14737.pdf (date of access: 23.10.2019).

22. Sharovarov D. (2015). Sila intellekta dlya elektrosnabzheniya gorodov. URL: https://www.siemens.com / ru / ru / home / kompaniya / klyuchevye-temy / ingenuity-for-life / besk.html (date of access: 27.10.2019).

23. Renewable energy statistics (2018). Eurostat Statistic explained. URL: http://ec.europa.eu / eurostat / statistics-explained / index.php / Renewable_energy_statistics (date of access: 06.10.2019).

24. World energy outlook (2017a). IEA.org. URL: https://www.iea.org / weo2017 / #section-2–1 (date of access: 17.10.2019).

25. World energy outlook (2017b). IEA.org. November. URL: https://www.iea.org / weo2017 / #section-2–2 (date of access: 20.10.2019).

The Doctor of Economics, the head of the department “Renewables” of RGU of oil and gas (NIU) of I. M. Gubkin, the head of the department of PAO “Lukoil”. Research interests: transformation of power branch, risk management in power industry.

Zubakin V.A. STATE STIMULATION OF TRANSFORMATION OF POWER INDUSTRY. Strategic decisions and risk management. 2019;10(4):320-329. https://doi.org/10.17747/2618-947X-2019-4-320-329

Ligovsky av 73, of.401, Saint Petersburg, 190040, Russia

Tel.: +7 (812) 346-50-15 (16)

Real Economy Publishing House.

E-mail: info@jsdrm.ru

Registration certificate PI No. FS-77 - 72389 from 02.28.2018, issued by the Federal Service for Supervision in the Sphere of Communications, Information Technologies and Mass Communications.

Processing of personal data