Contents

Scroll to:

https://doi.org/10.17747/2078-8886-2018-3-88-107

Scroll to:

The first attempts to create devices that allow interacting with the imitated reality, as well as augmenting reality with superimposed information, were made at the beginning of the 20th century, the very concept of mixed reality (the “reality-virtuality continuum”), which elements are virtual (VR) and augmented (AR) reality, is quite young (24 years), as well as the market of these technologies. The concept of virtual and augmented reality hasn’t changed radically in the past 30 years, but VR and AR devices and software, and content have gone through a significant evolutionary path, and have already experienced several growth spikes.

VR and AR technologies can be applied not only in entertainment and games. Many experts believe that virtual and augmented reality, along with Big Data, cloud technologies, artificial intelligence and some others, will become the key technologies of the 4th industrial revolution. VR and AR also have the potential to become the next big computing platform. Today VR and AR technologies help not only to create conceptually new markets, but also to disrupt existing ones.

This article discusses the evolution of the VR and AR concepts and technologies and current market trends. The results of the survey show the key obstacles for the mass distribution of AR and VR technologies: high implementation and operational costs of AR/VR solutions; lack of high-quality content and imperfect devices, implicit effectiveness of their use.

Based on the empirical study, a rather extensive list of benefits from using virtual and augmented reality technologies has been drawn up: faster and cheaper learning, training and guiding processes, increase in their efficiency, the reduction of the costs of elements and supplies needed, training support personnel; reducing potential risks to life and health of employees and other people while special training (medical operations and invasive procedures, evacuation, security, rescue in various emergencies) and the related optimization of the compensations; reducing the number of errors and accelerating the processes of assembling, repairing and operating special equipment, searching for information, necessary details, product location in the warehouse; significant reduction of accidents rate, as well as the exploration costs, due to the early identification of malfunctions; accelerating the pace of the designing and prototyping objects, significantly reducing the cost and duration of physical modeling process; improving customer experience, product and trading platforms design, that leads to corresponding increase in volume of sales; improving (simplifying) of communication and increasing its effectiveness.

Ivanova A.V. VR & AR TECHNOLOGIES: OPPORTUNITIES AND APPLICATION OBSTACLES. Strategic decisions and risk management. 2018;(3):88-107. https://doi.org/10.17747/2078-8886-2018-3-88-107

Discussions about the augmented and virtual reality are held quite frequently. Both technologies are covered by the media, they become the objects of research; books and films about them are created.

A significant impact on the rapid development of augmented and virtual reality technologies was made by the mobile device market, which over the past 10 years has changed beyond recognition: touch-screen smartphones and tablets with a fully-featured operating system, equipped with powerful video cameras, positioning sensors and gyroscopes, replaced push-button devices [Trachuk A. V., Linder N. V., 2017]. The growing computing power of devices and the ubiquitous digital transformation have taken the augmented and virtual reality technologies to a fundamentally new level, where they can go beyond the entertainment industry and cover a wide range of new areas of human activity. Today, the technologies of virtual and augmented reality have become a source of technological capabilities contributing not only to the creation of conceptually new markets, but also to the expansion of the existing ones [Trachuk A. V., Linder N. V., 2017]. In addition to entertainment, the technologies of augmented and virtual reality are widely used for designing, training and retraining of specialists, software products for engineers, architects, designers, realtors and retailers.

The augmented and virtual reality technologies are used in education and medicine; training programs and simulators are developed on their basis; medical devices simulate and conduct medical operations. Related to the above, the relevant issue is the impact that the augmented and virtual reality technologies can have on business.

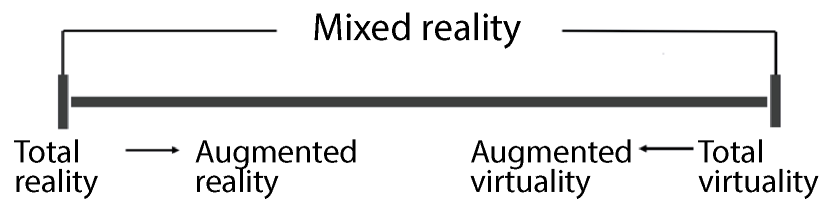

Fig. 1. Hybrid reality model [Milgram P., Kishino F., 1994]

The model of mixed (hybrid) reality, or the “reality-virtuality continuum” (Fig. I), was first described in 1994 [Milgram P., Kishino F., 1994]. The mixed reality is defined as a system in which objects of the real and virtual worlds coexist and interact in real time, within a virtual continuum. Intermediate links in this model are augmented reality and augmented virtuality. Augmented reality is closer to the real world, and augmented virtuality is closer to the virtual one.

The authors of the model have identified its main elements:

This study is focused primarily on the augmented reality and virtual reality. The fundamental difference between them is that virtual reality constructs a completely digital world, restricting the user access to the real world, whereas the augmented reality only adds elements of the digital world to the real one, modifying the user space.

In virtual reality the environment is created through a complex impact on its perception using virtual reality helmets or other technical means that dynamically update the user-visible space.

In the human brain neurons react to virtual elements as well as to the elements of the real world. Therefore, a person perceives the virtual environment and reacts to events occurring within the virtual world as if they occur in the real world [LaValle S. M., 2017].

The term “virtual reality” became popular in the mid-1980s; it was used and popularized by Jaron Lanier, an American scientist in the field of data visualization and biometric technologies, a pioneer in the field of virtual reality technologies and their commercial promotion.

These technologies appeared in the second half of the 20th century. Flowever, some experts believe that certain elements of virtual reality were described by scientists and philosophers long before that.

In our opinion, attempts to create a device that artificially recreates the conditions of the real world and at the same time has a complex effect on human perception can be considered the first step towards the creation of virtual reality technologies. In 1929 the Link Trainer flight simulator was patented. A moving picture was used as a visual image; navigation levers conveyed movement, rotation, falling, and course changes. Therefore, a satisfactory sensation of movement was created.

The ability to give the user the most realistic sensations, to immerse him in an artificially created world of sensations, is possible only with a complex impact on human perception. These effects were considered necessary for the development of the film industry in the 1950s [Heilig L.L., 1992]. In order to cover the traditional cinema screens with a glance a person needs only 5% of the field of vision. In general, the human perception by 70% (another 20% is hearing, 5% - smell, 4% - tactile sense and I % - taste) depends on the visual component. To create the effect of full visual immersion, it is necessary to use the entire 100% of the field of vision and, at the same time, to preserve the sharpness of image. Accordingly, to create absolute immersiveness, the same effect must be achieved with respect to other components of perception.

In 1957, on the basis of the Annenberg School of the University of Pennsylvania, Morton Fleilig created the world's first virtual simulator “Sensorama”, which looked like a slot machine with a dome and was a kind of 4D cinema for one user. Apatent for the device was obtained in 1962. The user could go on a virtual motorcycle ride through the streets of Brooklyn. The presence effect was achieved by affecting all the main senses at the same time: the screen showed the recording “in first person” shot simultaneously by three movie cameras, the seat vibrated, the fans created a feeling of headwinds, the stereo speakers transmitted the sounds of a busy street, the corresponding odors entered the room.

In 1967, Ivan Sutherland created the "Damocles Sword" - the first virtual reality helmet. Ahead-mounted display attached to the ceiling transmitted images generated on a computer. In addition, the helmet made it possible to change the generated images in accordance with the head movements.

The inventor noted that virtual reality devices were “a mirror to the mathematical wonderland” [Sutherland I.E., 1965]. An “ideal” display (a wearable device) connected to a computer gives a chance to get acquainted with ideas that are not realized in the physical world. The limit of development of this technology will be a device with the help of which a computer will be able to control the existence of matter.

The inventions Heilig and Sutherland had no commercial success, but served as the basis for subsequent developments. Their ideas inspired Andrew Lippman, who in 1978, together with colleagues at MIT and his team, created the first interactive map of Aspen (Colorado). It made it possible to take a virtual tour of the city by car.

In 1972, Myron Kruger coined the term “artificial reality” in order to determine the results that can be obtained by using a system of overlaying a video image of an object (person) on a computer-generated image and using other tools developed by that time [Krueger M. W., 1983].

In the 1980s virtual reality technologies were used in a number of NASA projects, for example, to create a virtual reality helmet. VPL Research Company created virtual reality glasses EyePhone and a touch-sensitive suit DataSuit capable of analyzing head and body movements and transmitting them within a controlled computer simulation.

In the 1990s virtual reality technologies were applied in the gaming industry. In 1993 Sega Corporation developed the Genesis console - a gaming platform using virtual reality technologies.

Unfortunately, the imperfection of the graphics and hardware components led to the users having nausea and dizziness as side effects. Because of this the console never went on sale. Their high cost led to the temporary abandonment of virtual reality technologies.

The first attempts to realize the augmented reality were made in the beginning of the 20th century. Even during the First World War aviation used collimator sights - optical devices combining a natural image of a target with a superimposed image of an aiming mark projected into infinity.

The term "augmented reality" was first proposed by Tom Caudell in 1992 describing digital displays that were used in the construction of aircraft. Assemblers carried portable computers and could see drawings and instructions with the help of helmets having translucent display panels [Caudell T.P, MizellD.W., 1992].

In 1992 Lewis Rosenberg developed one of the first functioning augmented reality systems for the USAF. The exoskeleton of Rosenberg allowed the military to virtually control the machines from a remote control center.

In 1994 Julie Martin staged the play “Dancing in Cyberspace”, where acrobats and dancers were immersed into a virtual environment by projecting virtual objects onto the stage.

In general, in the 1990s and 2000s the developments in the field of augmented reality were often associated with the creation of air navigation. For example, the task was to automatically determine the direction of movement depending on the goal chosen by the pilot, while the indicators showed relevant information against the background of the observed external situation. In other words, the real objects observed by the pilot in real time were accompanied by additional information.

In 1997 Ronald Azuma formulated the main criteria of augmented reality: combination of the real and virtual worlds, real-time interaction, displaying in 3D-space. Azuma believed that it was wrong to limit the concept of AR to certain technologies (devices), for example, glasses. In addition to adding some elements of the virtual to the real, within the framework of augmented reality it was also possible to remove the elements of the real [AzumaR.T., 1997].

In the early 2000s developers of the augmented and virtual reality technologies turned to the entertainment industry. In 2000, due to the augmented reality technologies it became possible to chase monsters along real streets in the video game Quake. This required a virtual helmet with sensors and cameras, which did not contribute to the popularity of the game, but it became a prerequisite for the appearance of the well-known PokemonGo.

In the 2010s the augmented and virtual reality technologies took another step towards the consumer audience. On August I, 2012 a little-known startup Oculus launched a campaign to raise funds for the production of a virtual reality helmet on the Kickstarter platform. The developers promised users a “full immersion effect” by using displays with a resolution of 640 by 800 pixels for each eye. In 2014 Google Corporation began the testing of GoogleGlass - a mini-computer integrated into a spectacle frame. In 2016 Microsoft Corporation introduced HoloLens - smart glasses for working with augmented reality. These events contributed to the active continuation of works in the field of the augmented and virtual reality technologies. Thus, after analyzing the history of development of these technologies, it can be noted that they have a lot in common:

Augmented reality combines the real and virtual worlds, complements the real world and expands its perception. Virtual reality, of course, is completely virtual. It replaces the real world, strives for absolute immersiveness (the effect of complete immersion).

Although the notions and concepts of virtual and augmented reality have not undergone radical changes over the past 30 years, the same cannot be said about the technologies themselves. The augmented and virtual reality technologies have gone through a significant evolutionary path in terms of improvement of devices, software and content. Listed below are the options for virtual and augmented reality devices currently on the market.

Virtual reality devices. Helmets and goggles (Head Mounted Display, HMD). In the helmet in front of the user's eyes there are two displays with the blinders protecting against external light, stereo headphones, built-in accelerometers and position sensors. The displays transmit stereoscopic images slightly shifted relative to each other providing a realistic perception of the three-dimensional environment. Most of the advanced virtual reality helmets are rather cumbersome, but there are also some simplified light options (including those made of cardboard), which are usually designed for smartphones with virtual reality applications. Virtual reality helmets are divided into three types:

Virtual reality rooms (Cave Automatic Virtual Environment). Images are transmitted directly on to the walls of the room, most often these are Motion Parallax 3D displays (with their help the user has the illusion of a three-dimensional object, since the screen displays a special projection of the virtual object generated depending on the user's position relative to the screen). Sometimes 3D goggles or even helmets are used to create the effect of total immersion in such rooms. Some experts believe that this kind of virtual reality is more perfect, since the displays make it possible to display virtual elements in higher resolution, there is no need to put on bulky devices and get tangled in wires, there is no motion sickness, self-identification is simplified, because the user constantly sees himself.

Auxiliaity headsets. Information gloves and joysticks help one better recognize the user's position in space as well as his actions.

Other devices. They include various foot platforms (3DRudder) and treadmills (VirtuixOmni). The user has the ability to control the movement of his legs, and in the case of the treadmills he can even move in space without the fear of encountering obstacles in the real world.

Augmented reality devices. Smart goggles and helmets. With the help of computer vision technology autonomous and compact devices with built-in sensors and cameras make it possible to analyze the environment around the user, to form a map of the space for orientation in it.

Most goggles are equipped with the function of voice and movement recognition, they can be controlled without using one’s hands. Images are projected on the lenses of goggles or special mini-displays, there is no need in additional tags to generate content. There are binocular (Hololens, DAQRISmartGlasses, Meta 2) and monocular (GoogleGlass, Vuzix M3000) models of goggles and helmets.

Mobile devices. Virtually any modem smartphone or tablet can become an augmented reality device, it is only necessary to install the appropriate program. As markers for object recognition one uses the marker technology, QR codes, generated endpoints, logos, computer vision and face recognition.

Interactive stands and kiosks projected in augmented reality. The tool is widely used in sales, at various exhibitions. Stands and kiosks are wide-format screens that make it possible to photo-realistically display visualized objects in a specific context (for example, a demonstration of certain functions of the product), to view information in an interactive mode. The image is superimposed on any surface (object).

It should be noted that today the market of augmented and virtual reality technologies is only beginning to develop, and the application of technologies will not be limited by the sphere of entertainment and games. Today projects with their use help not only to create conceptually new markets, but also to expand the existing ones.

Intheir 2016 study representatives of Bank of America Merrill Lynch state that, along with BigData, cloud technologies and artificial intelligence, augmented and virtual reality technologies will become the key technologies of the fourth industrial revolution, may become a key factor in the next-generation computing platform. A turning point in the development of these technologies is expected in 2020 [Future Reality, 2016].

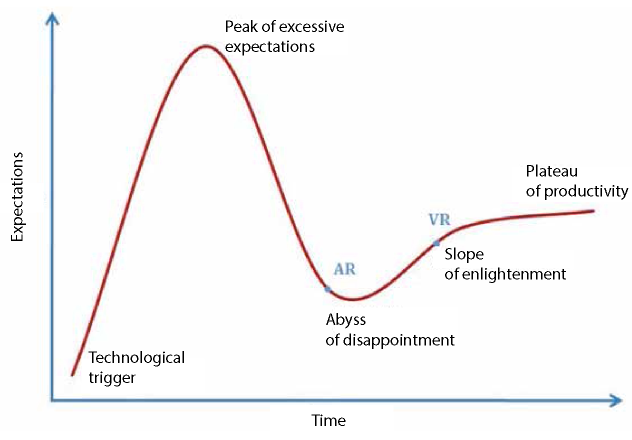

Fig. 2. The Hype cycle of technologies [Panetta K., 2017]

The consulting and auditing company PricewaterhouseCoopers annually conducts a study of the digital competence index among companies investing in digital technologies, 10% of companies invest in augmented reality (in Russia - 15 %), and 7 % - in virtual reality (in Russia - 9%). In three years 24 and 15% of the surveyed companies will be ready to invest in these technologies, respectively [Digital Decade, 2017].

According to the study conducted by PricewaterhouseCoopers, compared to other actively developing areas (Internet of things, artificial intelligence, robotics, 3D printing), virtual and augmented reality technologies will have a less destabilizing effect on their industries and business models.

Gartner Corporation, one of the major players on the IT analytics market, annually does a Hype cycle of technologies [Panetta K., 2017]. The graph of the Hype cycle (Fig. 2) shows technologies in accordance with their current position in time and the level of user expectations.

As can be seen, the technology of augmented reality is almost at the very bottom of the “abyss of disappointment”. This can be explained by the discrepancy of expectations according to the results of testing of devices and software products for augmented reality that came on the market. At this stage technology deficiencies are usually identified.

Virtual reality has gone through the “abyss of disappointment” and is currently on the “slope of enlightenment”. It has a stable audience. Developers are launching its commercial implementation and are actively looking for solutions to the existing problems.

According to some forecasts, the virtual reality technology will be introduced in about 2-5 years, the augmented reality technology - in 5-10 years.

It is interesting to compare these results with the previous periods. For example, in 2011-2012 the technology of augmented reality was at the top of the “peak of excessive expectations”, and the virtual reality technology was at the bottom of the “abyss of disappointments”, as the augmented reality is today.

If we analyze the maturity cycle of other technologies (for example, smartphones, voice and biometric recognition, app stores, etc.), then we can conclude that the forecast of Gartner is sufficiently accurate. Therefore, these studies can be regarded as a vector of technologies.

The technologies of virtual and augmented reality are becoming increasingly popular in companies. In the near future the augmented and virtual realities will bring changes to the established business processes and tasks generating fundamentally new experiences [Kunkel N., Soechtig S., Miniman J. et al., 2016] (Table I).

Today, the development of content and software for the virtual and augmented reality can be compared with the development of mobile applications. The market has end-product developers and business tools based on these technologies.

The content and software can also be divided into two types:

о training and skills development;

о prototyping and visualization;

о assistance in the operation of equipment;

о communications.

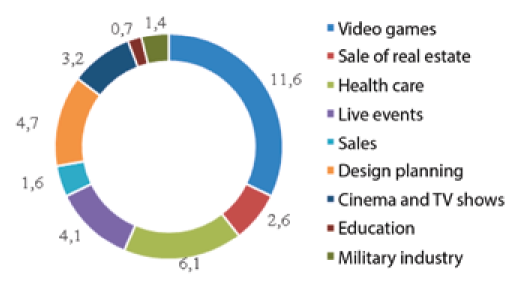

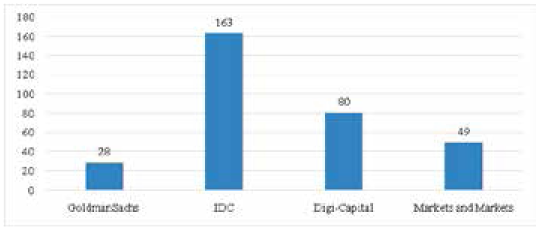

In 2016 the investment bank GoldmanSachs conducted a global analysis of the market of virtual and augmented reality technologies, made a forecast of the market potential in 2020 and 2025 in various areas of activity [Profiles, 2016]. According to the experts, the total volume of the software market for virtual and augmented reality in 2025 will amount to 35 billion US dollars, and the total audience - 315 million users (in 2017 the market volume was about 9,1 billion dollars. [World market, 2017]).

Experts came to the conclusion that, in addition to entertainment, in the near future virtual and augmented reality technologies will be widespread not only in the field of entertainment, but also in real estate, commerce and healthcare (Fig. 3). Analysts believe that the share of software in B2C segment will be 54%, and in B2B segment - 46% [Profiles, 2016].

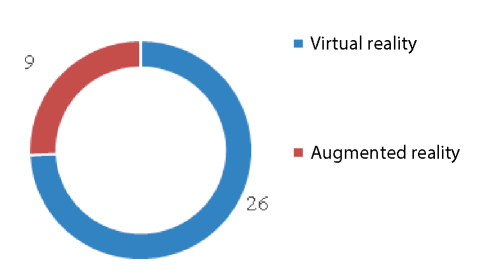

The development of software and content for augmented reality will significantly lag behind the same for virtual reality, and by 2025 three-quarters of the market will belong to the solutions for virtual reality (Fig. 4). However, over time, this gap will diminish [Profiles, 2016].

Table 1

The use of technologies of virtual and augmented reality [KaiserR., Schatsky D., 2017]

|

What? |

Where? |

Potential results |

|---|---|---|

|

Management and interaction |

||

|

Visual cues to help workers perform the tasks of maintenance, repair and assembly |

Aerospace industry, military industrial complex, automobile industry, construction, healthcare, oil and gas industry, energy and utilities, technical and applied sciences |

Increased productivity, streamlined workflow, risk reduction, remote interaction |

|

Immersive learning |

||

|

Creation of realistic environment for training, which in normal conditions is associated with high risks or high costs for employees; reproduction of certain conditions and phenomena for the purpose of psychological rehabilitation |

Consumer segment, healthcare, higher education / training programs, industrial products |

Reduction of risks, reduction of costs, increase in therapeutic effect, saving of consumables |

|

Improvement in customer experience |

||

|

Improvement in customer experience by implementing customizable and unique methods of interacting with a company, brand, or product |

Automobile industry, banking and securities, consumer products, media and entertainment, tourism, services |

Customer involvement, increased marketing opportunities, growth of sales, increased brand competitiveness |

|

Design and Analysis |

||

|

Data visualization, design planning, new forms of analysis |

Aerospace and military industrial complex, automobile industry, construction, higher education, real estate, technical and applied sciences |

Cost saving, increased efficiency, identification of design errors on the early stages, new methods of data analysis, reporting and forecasting |

Fig. 3. The share sales of the virtual and augmented reality software by 2025, billion dollars. [Profiles, 2016]

Fig. 4. Forecast of the market of software for the virtual and augmented reality in 2025, billion dollars. [Profiles, 2016]

According to the forecast of GoldmanSachs, virtual reality devices will soon become as popular and functional as mobile phones. With the help of such devices users can watch movies and TV shows, attend mass events and make purchases. This means that virtual reality will significantly expand the capabilities of small and large businesses.

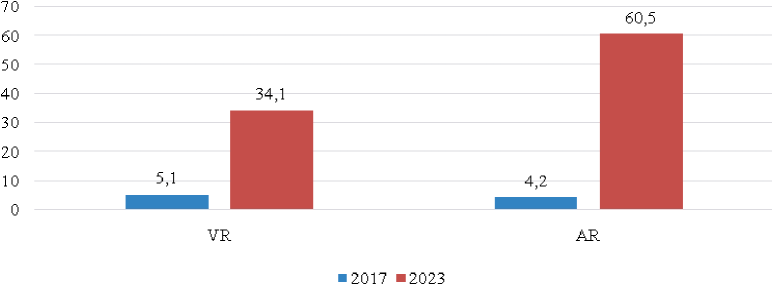

The forecasts of other companies differ from those presented in the study of GoldmanSachs. It is expected that the total volume of the market of hardware and software for virtual reality technologies in 2023 will increase to 34,1 billion dollars, and for the technologies of augmented reality - to 60,5 billion dollars [Augmented Reality, 2018] (Fig. 5).

The key driver of growth in the market volume of virtual reality devices will be the proliferation of virtual reality helmets thanks to the gaming and entertainment industry.

Significant growth in the field of augmented reality technologies, the prevalence of augmented reality technologies over virtual reality technologies are primarily caused by the growing demand for augmented reality devices in the health sector, significant demand is predicted for indicator systems that are projected onto windshields, ready-made software solutions with augmented reality for sales, growth in investments in the creation of augmented reality devices.

Fig. 5. Forecast of the market of technologies for the virtual and augmented reality, billion dollars. [Augmented Reality, 2018]

In addition, the popularity of augmented reality can be explained by the following factors:

Analysts believe that the market for augmented reality devices will grow faster than the market for virtual reality devices, and in three years augmented reality will become one of the main technologies [After mixed year, 2017]. A significant share of growth on the market of those and other technologies will be due to the development of software in B2C segment and hardware. By 2021 mobile devices of the augmented and virtual reality (approximately 75% and 16%) will be the most popular; the remaining share will be equally divided between wearable devices of virtual and augmented reality [After mixed year, 2017].

In general, the forecasts for the future of 2020 vary, but the tendency to manifold growth can be traced in all these studies (Fig. 6).

Regarding the players on the global market, depending on their functions, the following categories can be distinguished:

Fig. 6. Forecast of the volume of revenues on the market of technologies of virtual and augmented reality by 2020, billion dollars.

Fig. 7. Increase in the user base of the main platforms of virtual reality in Russia, mln. dollars., in 2016-2020 [Market, [2017]]. An asterisk denotes a prediction.

Based on the analysis of the relevant categories The Venture Reality Fund made a map of the global market of virtual and augmented reality.

The year 2017 was decisive for the VR industry: consumer versions of special headsets from Oculus, HTC, Google and Sony were released, and many large video game publishers and studios released or announced games of various genres and formats for virtual reality. In many countries, including Russia, the first industry associations were created in order to consolidate marketing and intellectual assets, to develop common technological standards.

Some Russian companies are actively exploring the possibilities of using the augmented and virtual reality technologies in business. The fact that companies are ready to use them is evidenced by the creation in 2015 of the Association of Augmented and Virtual Reality and in 2016 the country's first VR consortium, in which the largest technology and media companies united their competencies.

The same tendencies are observed in Russia and other countries [Market, [2017]]. Moreover, the analysis of developments on the Russian virtual reality market in 2017 makes it possible to forecast that Russian companies can claim a prominent place on the global market of virtual reality technologies (Fig. 7).

Fig. 8. Structure of the Russian B2B market of virtual reality technologies by project areas [Market, [2017]]

By the end of 2016 the Russian consumer market of devices, software and content for virtual reality was estimated at 21,7 million dollars, while the market of B2B solutions - at 6,2 million dollars.

The main customers: high-tech public and private companies and major brands. The main developers: large IT integrators developing complex solutions in the field of virtual reality, small creative studios engaged in the development of installations in the form of virtual reality. In 2016 the number of companies in the segment of virtual reality technology increased significantly from a few dozen to more than a hundred. The market has more than three hundred small (up to 5 people) creative teams that produce and actively promote the content and virtual reality solutions [Market, [2017]].

The largest Russian companies are beginning to be interested in virtual reality technologies. So far only a few have introduced them into their business, but in 2016 the number of such enthusiasts more than doubled, which means that one can optimistically assess the trend on the Russian market.

One of the key factors that influenced the formation of the Russian market was the growth of investment volumes: in 2015- 3.4 million dollars, in 2016-13 million dollars. By the end of 2016 the Russian market of business-oriented solutions in the field of virtual reality was estimated at 6,2 million dollars (Figure 8). The main drivers of the market in Russia are virtual reality technologies for mobile devices and the development of content for viewing video in 360 ° format and undemanding technical characteristics. In general, it can be concluded that technologies are rapidly developing and have already experienced several growth spikes.

Today, companies and investors continue to invest millions of dollars in technologies of the virtual and augmented reality, but the technologies themselves have not yet become widespread. There are certain problems in the development of virtual and augmented reality technologies:

The widespread proliferation of the augmented and virtual reality technologies is hampered by a number of shortcomings identified during their active testing and use. So far it has not been possible to fully eliminate these shortcomings (Table 2).

Among the common problems one can identify high costs of wearable devices (helmets and goggles). If not every ordinary user can afford a virtual reality helmet, then even some companies cannot afford augmented reality smart goggles.

The same situation can be observed in the field of specialized software. Custom solutions will cost a lot of money to business, especially if they go beyond the standard ones or are developed for highly specialized areas and should take into account a number of industry-specific features.

Acommon problem is imperfection of devices and software. The current level of technological development does not allow to realize the full potential of augmented and virtual reality. One of the properties of the virtual reality is immersiveness. However, the effect of full immersion is impossible to achieve due to the low resolution of displays, low mobility of devices and insufficient productive capacity of platforms (PC, console).

In the augmented reality the main problem of devices is no longer connected with the resolution of the picture, but with the viewing angle. For mobile devices the visible area of augmented reality is limited to the screen of a smartphone or tablet, and the largest viewing angle is 90 ° (Meta 2).

The issue of information security has not been resolved yet. By themselves, the augmented and virtual reality devices do not have a mechanism to protect personal and confidential data. Therefore cybersecurity tools will have to be searched for and purchased separately.

Insufficient adaptation of content for a specific platform or device is relevant for both types of reality. What works with Apple does not work with Android. The same is true for HTCVive and Playstation VR. Not all AR and VR programs are cross-platform, which significantly reduces the possibilities of their use.

However, many experts believe that technologies of the augmented and virtual reality have great long-term prospects, and many of the shortcomings will be eliminated in the next five years. According to J. Richitello, CEO of Unity, which created a cross-platform environment for the development of computer games, in 2018-2019 it will be necessary to reduce the costs and increase the functionality of virtual reality devices [5 Conclusions, 2017]. This statement, in principle, meets the expectations of Gartner Company (see Fig. 2): virtual reality technologies will be ready for widespread use in the next 2-5 years.

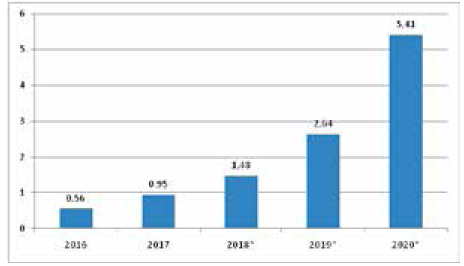

Summarizing, we can say that the market for technologies of virtual and augmented reality is rapidly growing and developing. In 2018, an increase in the volume of the augmented and virtual reality market is expected to be almost 95% compared with 2017; by 2020 the market will grow manifold (according to various forecasts, from 3 to 18 times).

Table 2

Classification of the existing shortcomings of the virtual and augmented reality technologies

|

Category |

Virtual reality technology |

Augmented reality technology |

|---|---|---|

|

Hardware |

• Heavy and uncomfortable helmets, big headsets • spatial constraints when moving; • inability to repair on site; • Ingh costs; • insufficient display resolution |

• Small viewing angle; • inability to repair on site; • Ingh cost of wearable devices, direct correlation between performance and cost |

|

Content |

• Lack of quality content • errors in scientific accuracy when transferring real objects and phenomena into the virtual world; • poorly developed world (lack of integrity, incorrect spatial relationship between the elements), bugs; • technical limitations; • Ingh costs of specialized content |

• Lack of quality content; • errors in scientific accuracy when transferring real objects and phenomena into the virtual world; • technical limitations; • Ingh costs of specialized content |

|

Software |

• Dependence on PC performance and consoles; • deficiency of graphics; • lack of direct compatibility with platforms and integration with other programs; • poor content optimization, poor performance; • lack of prompt error elimination |

• Errors of object recognition; • incorrect display of overlaid data; • incorrect location of objects in space; • incompatibility with platforms, lack of integration with other programs; • low productivity; • bugs, insufficiently prompt elimination of errors |

|

Security |

• Lack of a mechanism to protect personal data and confidential information; • malware |

• Lack of a mechanism to protect personal data and confidential information; • malware |

|

Impact on user |

• Nausea, dizziness, headache, eye strain; • load on the neck and spine; • loss of orientation, sense of time, reality; • collision with objects of the real world, risk of injury |

• Distracted attention, loss of focus, fatigue; • risk of injury |

Most analysts give preference to the augmented reality, because it has more opportunities for application, is simpler to develop and easy to transmit through mobile devices. So, according to experts, the greatest market growth will be provided precisely by the augmented reality for mobile devices.

The virtual reality will capture the niche of games and entertainment and B2B segment, while solutions of the augmented reality will find wide application in B2C segment.

These technologies open up new opportunities in the field of modeling and data visualization, navigation, design planning, training and retraining, the formation of customer experience and communications. They can be useful for companies in various industries such as health care, education, retail, real estate and construction.

Semi-structured interviews were conducted in order to study the experience of using AR/VR technologies and their influence on the processes in Russian companies. Questions about the application of new technologies were formulated based on the results of research [A. Trachuk, V., Linder, N. V., 2016; 2017a; TrachukA., Linder N., 2017]. Questions about the factors that impede the use of technologies were formulated on the basis of the research [A. Trachuk, V. Linder, 2017 b]. We searched for informants among friends and acquaintances, among the members of communities dedicated to technologies of the augmented and virtual reality, in social networks (Facebook, VKontakte). 35 people were interviewed: representatives of both sexes as respondents - 19 men and 16 women, mostly under the age of 35 (85,8%). Fields of professional activity: entertainment, games, education, IT, marketing, public service, medicine, sociology, finance, logistics, automation, aerospace, electric power, journalism.

Informants included the respondents who:

Respondents were asked to be interviewed by using the online application Google Forms. The choice of the interviewing format was caused by inability to conduct face-to-face meetings and conversations with respondents due to various circumstances.

The questions were grouped into three blocks:

The last two blocks contained questions in answering which it was necessary to choose one of several options or give a detailed answer. If the forms are filled out poorly, one has to discuss the answers at the third stage in order to supplement and clarify them. Communication with respondents was carried out through voice or text chat in instant messengers (Facebook, VKontakte, Telegram, Discord).

Special attention was paid to the discussion of the following issues:

For a deeper understanding of the results a case-study method was used with a SWOT analysis conducted to systematize the data obtained during the previous stages of the study, the weaknesses and strengths of the augmented and virtual reality technologies, their applicability and threats that companies may encounter, were identified.

In general, the majority of respondents are optimistic about these technologies (positive responses were made by 71%). From an emotional point of view, the experience of use is described as “useful”, “necessary”, “changing the idea of the future”, “exciting”, “effective”, “meaningful”, “interesting”, “having the potential”, “without prospects for further use in the near future ","generally entertaining, but hardly realizable", "not justifying the costs".

The activities of three respondents are directly related to the development of software (content) in the field of entertainment using the augmented and virtual reality, another respondent sells ready-made solutions (also in the field of entertainment and games). Another 22 respondents used augmented and virtual reality in their work: more than once - only 13 people, use on a regular basis - 3 people. Six respondents expressed their opinion about the possibility of introducing the technologies at the present time, another 18 considered that in Russia these technologies would be widely available not earlier than in 2024- 2025.

Nine respondents did not deal with the augmented and virtual reality in their work, but five of them see the potential of technology in their field of activity (in education, medicine and sociology).

The exception was the field of finance: both representatives noted that they did not see prospects for the use of augmented and virtual reality solutions in financial analysis, while one of them believes that augmented technologies may be useful when training in specialized programs.

Nine people believe that their industry is ready for the implementation of these technologies today (education, sales, logistics, automation, aircraft manufacturing, sociology and psychology). Thirteen respondents noted the high potential for the use of technologies in the near future. Three persons are dubious about the development of the Russian B2B segment in the near future explaining this by unfavorable institutional environment and the lack of the necessary infrastructure.

The most optimistic forecasts were given by respondents working in large commercial companies. Representatives of medium and small enterprises as well as those people working in the public sector and budgetary institutions, showed restraint. This is easily explained, because in the early stages the adoption of technologies requires great courage and big investments. However, when technologies are widely implemented, it is the small and medium business that will benefit most from their use, since the benefits, for example, those leading to the significant reduction in transaction costs, will exceed the costs of implementation.

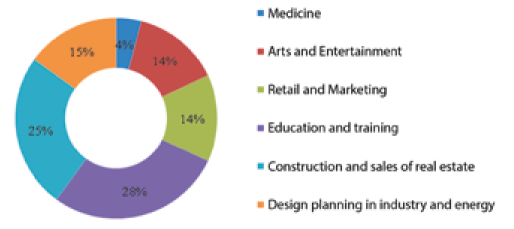

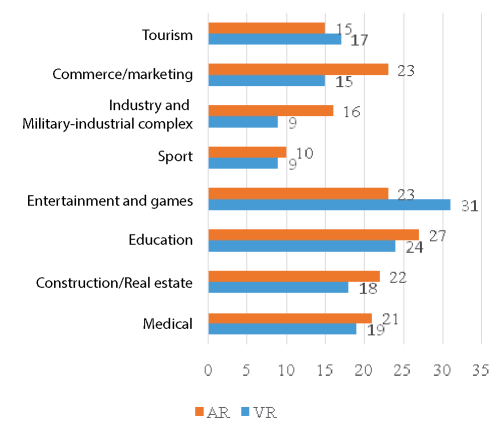

In addition to entertainment and games, respondents named other promising areas for the introduction and application of technologies: education, medicine, construction and real estate, commerce and marketing (Fig. 9). The superiority of the virtual reality over the augmented reality is observed only in the fields of entertainment, games and tourism that are of greater interest to consumers.

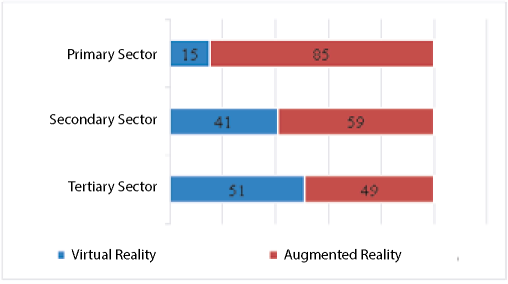

Such results confirm the expectations of most experts: the augmented reality due to its peculiar features (device autonomy, convenience and ease of wearing, access to the real world) has great application prospects in all sectors of the economy (starting with the extraction of raw materials and ending with the service industry) (Fig. 10 ).

Fig. 9. Promising areas for the application of virtual and augmented reality technologies, units, according to the respondents' answers

Fig. 10. Application of technologies in three sectors of the economy, %, according to the respondents

The examples described mainly the cases with simulation of situations in training conducted in virtual reality. Thetechnologies of augmented reality were mainly used to optimize production processes and visualize information. Here are some examples:

It is important to note the qualitative results of the use of virtual and augmented reality technologies, their influence on the workflow, which were highlighted by the respondents during the interview:

о reduction of training and instructing time, increase in their efficiency due to visibility and interactivity of information, greater involvement of participants in the process;

о reduction of the costs of consumables required for training;

о reduction of the costs of trainers and increase in the number of persons undergoing training; о prevention of potential risks: if situations are simulated in advance (medical operations and invasive procedures, evacuation, provision of security, rescue in various emergencies), one can avoid potential threats to the health and lives of employees and other people during training and instructing, and for companies — compensations and insurance payments;

о reduction of time spent on the search of goods in warehouses (the area with the necessary goods is highlighted);

о reduction in the number of errors and time spent on assembling, repairing and operating special equipment (interactive step-by-step instructions and graphic prompts are displayed, there is an error indication); о assistance in management and ensuring safety during air and space flights, sea transportation, operation of military equipment, vehicles (safety and “comfort” of movement and operation are ensured through environmental analysis and relevant navigation prompts, as well as monitoring of the state of technical systems (full step-by-step technical support in the process of error elimination); о accident rate is significantly reduced along with the costs of operation of equipment due to the timely detection of trouble;

о testing (crash testing) of equipment and machinery (cost saving);

о modeling of production stages — increase in labor productivity, reduction of errors; о reduction of time in designing facilities, communication systems, (identification of errors at the early stages, the ability to update information about the readiness of facilities in real time);

о increase in revenues due to improved customer experience (using the application a consumer can get detailed information about the product, its characteristics, brand, “try on” things in an electronic fitting room, find out how the interior/furniture elements will look like, how the finished product will function) and attract new users (creating a wow-effect);

о reduction of rental space (there is no need to store the entire range of products in each outlet);

о support of analysis of customer behavior in the store, on the basis of which the design of stands and merchandising are improved affecting the volumes of sales;

о formation of a more accurate picture of the final product (the development process is simplified, the time and financial costs of consumables and visualization are reduced);

о building of business relationships (training of employees in the skills of business communication and interaction with colleagues, partners and customers);

о remote interaction with all departments regardless of their geographic location, simplification of the communication process, reduction of travel expenses, participation in seminars and meetings;

о more effective interaction within the team by involving all employees in the process of discussion, work, problem solving;

о faster and more effective patient treatment (fighting phobias, PTSD, pain relief, elimination of anxiety), which is a competitive advantage making it possible to set higher prices for services.

Таblе З

Risks of implementation and use of the augmented and virtual reality technologies

|

Risk |

Causes |

Consequences |

|---|---|---|

|

Risk of insufficient awareness |

Lack of reliable information on the results of implementation and application of technologies of the augmented and virtual reality in other companies |

Increase in operational costs and staff training costs, longer payback period, loss of investments |

|

Technological risks |

Damage to (malfunction of) the device and components, imperfection of devices (inconvenience of wearing, small viewing angle), unsuitable environmental conditions (for example, the contrast of overlay images in smart augmented reality goggles depends on the room illumination), low resolution of the image, problems of object recognition, incorrect displaying (design) of objects |

Suspension of the work process (delays), loss of possible benefits, costs of repairing / purchasing of the device, inability to use all the possibilities of technology |

|

Rejection by employees |

Lack of understanding of the principles of operation of devices, low awareness, fear of losing work |

Increase in monetary and time costs for training and informing employees, revision of management policies and systems of motivation and employee involvement, possible staff reductions (extreme case) |

|

Imperfection of (lack of) content |

Lack of the necessary programs or their timely updating, bugs |

Suspension of the work process (delays), inability to use the augmented and virtual reality devices |

|

Information security |

Information leakage, hacking into the system |

Loss of data, loss of profits, the costs of developing/ purchasing security solutions |

|

Injuries and negative health effects |

Collision with objects of the real world, nausea and dizziness, eye strain, psycho-emotional stress. |

Increase in the number of claims for compensation payments, impossibility of prolonged use of devices |

|

Dependence on related technological areas |

Insufficient power of the shared equipment (PCs, consoles, smartphones, displays) |

Rising logistics costs |

Thanks to the respondents' answers it was possible to ascertain the benefits of using technologies of the augmented and virtual reality, although this list is obviously not complete, since the respondents work in several industries. Some benefits, such as simplifying and increasing the efficiency of learning and communication processes, are fairly universal and can be useful for any company. Based on the obtained data the study analyzes the prospects of B2B market for the virtual and augmented reality technologies in Russia.

Some risks may arise in the process of implementation and use of the augmented and virtual reality technologies (Table 3). In general, most of the risks are acceptable and do not have serious consequences for the company. Although, depending on the scale, some risks may become critical for small or new companies (loss of investments).

In the process of making a balanced and correct decision about the implementation of augmented and virtual reality technologies an important role is played by the existing risk management policy in the company. Effective risk management will help avoid or minimize the consequences of risk occurrence.

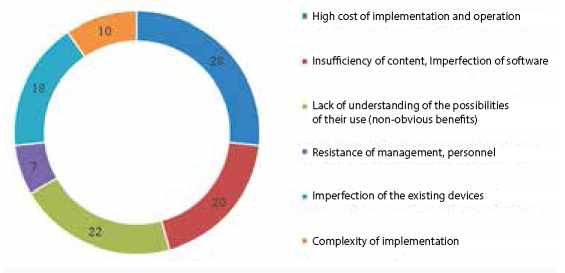

The respondents also identified a number of factors that, in their opinion, considerably impede mass distribution of these technologies (Tig. 11). Most of the factors named by the respondents are the consequence of the existing technology deficiencies (see Table 3). Therefore, the respondents believe that mass distribution is impeded by:

Fig. 11. Factors preventing the proliferation of the augmented and virtual reality technologies.

Table 4

The results of using VR in preparation of the Winter Olympics in 2014

|

Opportunity |

Result |

Effect |

|---|---|---|

|

• 3D-design; • integration of a three-dimensional model with data from other systems of the operator; • reflection of data and characteristics of objects; • the ability to view objects from the inside; • positioning and relocation of objects; • creation of all kinds of marketing materials; • simultaneous work of multiple users; • remote access; • separation of access rights and division of work into areas; • the possibility of со-viewing; • registration of all introduced changes in real time; • access to all versions of the project; • visualization of user notes to objects; • online interaction of units; • formation of reporting; • the ability to navigate objects; • the ability for people to interact with objects, to perform specific actions |

• Creation of a model that combines architectural, planning and engineering solutions with a reflection of all technical and economic indicators; • identification of deficiencies of objects at the designing stage; • verification of operational hypotheses long before physical implementation of the construction object; • estimating each object; • development of facilities, territories and infrastructure on a "turnkey" basis; • development of sponsorship programs; • no need for the physical presence of all employees at facility, on the same territory; • demonstration of facilities to colleagues, partners, investors and other interested people; • reporting to decision makers; • interaction within a single model without loss of confidentiality of information for each object; • training of staff and volunteers (development of routes); • training of specialized personnel (security and safety), drills of actions during certain situations; • study of the territory, location and internal structure of objects |

• Reducing the number of errors; • reducing the duration of planning and creation (development) of objects; • cost saving on physical modeling (mockups); • reducing the duration and costs of finding the best design solutions at all stages of games preparation; • savings on personnel costs (subcontractors, designers, workers, marketers, training and management personnel) • savings of time and costs for the acquisition and positioning of objects; • simplification and cheapening of communications between all project participants (contractors, sponsors, organizers, service workers, volunteers, etc.); • simplification and cheapening of reporting; • attraction of additional investments; • acceleration of interaction between employees of departments; • possibility of training in relation to certain locations until the objects are commissioned; • reduced time for training and instructing; • reducing the costs of items and consumables required for training; • reducing the costs for the training of personnel |

Opinions on the main factors hindering the implementation of these technologies in Russian companies are collected. The expectations regarding the main trends and directions of development of these technologies in Russia in the near future are revealed.

Projects of the virtual and augmented reality technologies The obtained experience allowed the founders of NextSpace to later launch Revizto - a product that allows any company to use tools of effective management and collaboration in the development and information modeling of buildings by using virtual reality headsets and helmets. Revizto package solutions, similar to those implemented in the Olympic project, are used by more than 50 thousand users in 150 countries of the world.

On the company's official website one can see reviews given by customers (universities and museums, construction, designing and engineering companies, design studios, real estate agencies) [Team blog]. Each of them describes positive effects from the implementation of tools into their business, in particular, a significant acceleration of coordination at all stages of project implementation (up to 30%). Therefore, we can assume that the experimental results obtained during the implementation of the project “Virtual Sochi 2014” and the use of the Revizto software package prove the positive effect of virtual reality technologies on the processes within companies.

Let us consider examples of the use of the virtual and augmented reality technologies in Russian companies.

Virtual laboratory of augmented reality "My profession". By order of the Palace of Schoolchildren in Astana AR Production created the first museum in the world, in which all of exhibits are virtual. There are 30 interactive projects in the building (22 of them are projects at the junction of augmented and virtual reality technologies). Contrast marks are put on the walls. Thanks to the virtual reality goggles the user sees three-dimensional scenes with which it is possible to interact with the joystick. The museum has prepared educational and entertainment projects using the projected augmented reality. While playing a child can become familiar with major industries, for example, construct a building in stages or study alloys mixing their components in a smelting pot.

The opening of the laboratory made it possible to attract a new audience. This project clearly demonstrated that in education the use of gamification methods in conjunction with visualization of material using virtual elements allows to engage students more deeply in the educational process, to keep their attention and increase their motivation to learn. Therefore, the obtained knowledge and skills are better absorbed.

Visitors were invited to explore an interactive science park, nuclear energy information center, winter garden, planetarium, educational circles and programs, etc., which, accordingly, increase the institution’s revenues not only through the activities of the museum itself, but also due to the increase in new consumers in other projects [Interactive Museum],

Projected system of augmented reality (Light Guide Systems) in the workplace. At each stage of the assembly process workers receive visual information about the necessary actions (animated highlighting of objects, visual cues in the form of text, symbols, graphics, drawings or video), which is projected onto the working surface.

After the implementation of projection systems in various manufacturing companies the company Light Guide Systems monitors the results. For example, in the concern Fiat Chrysler Automobiles an experiment was conducted: operators were tasked to assemble gears and chains. The whole process was divided into 10 consecutive stages. Workers needed to select the necessary components, carry out the installation and make sure that everything was done without errors. Some operators followed standard paper instructions while others used augmented reality tools. In the latter case the following results were obtained:

The use of this projection system in the process of training at the Chrysler World Class Manufacturing Academy training center also revealed the following positive effects:

Similar results are observed by many users of the solution.

This proves that the identified results are not random [OPS Solutions, 2018].

* * *

We received a positive effect from the implementation of augmented reality in the production and educational processes from using it as a tool to attract new audiences and increase profits. The experience of implementing the technologies in general makes it possible to assess their potential for future use in business.

During the interviews and analysis of the use of technologies we obtained data that make it possible to identify strengths and weaknesses of technologies, their applicability and threats that companies may encounter. To systematize information obtained from interviews a SWOT matrix was built (Table 5).

The technologies of virtual and augmented reality have a number of advantages. Their capabilities are almost endless in education, medicine, science, sports, industrial use, as well as in the field of games, entertainment and other areas. Provided that the potential of these technologies is properly utilized, companies will be able to achieve the desired benefits by increasing employee productivity, improving work processes, attracting new customers and deepening the professional competencies of their employees.

The proliferation of virtual and augmented reality technologies is hampered by a number of factors, mainly related to technological deficiencies, but it can be expected that by 2020 significant deficiencies will be eliminated.

Together with parallel development of other digital technologies (BigData, blockchain, artificial intelligence, Internet of things), this will make it possible to create by 2030 a platform for active development and improvement of the augmented and virtual reality technologies. If device developers do not overestimate consumer expectations (as was the case with GoogleGlass) and potential content creators are not disappointed with these technologies, by 2025 it will be possible to talk about their full transition to the stage of stable commercial implementation.

The drivers of the market development as a whole will be knowledge, skills and competencies gained in the process of developing consumer solutions. In particular, in the field of virtual reality they will serve as a support for the development of the gaming and entertainment industry, and in the field of augmented reality - augmented reality technologies for mobile devices and head-up displays, as well as solutions in the areas of health, sales and e-commerce.

The key to successful implementation is the availability of innovators and early followers. It is very important that companies in different industries share their experience in technology implementation while projects in the field of augmented and virtual reality technologies are covered by the media and networks. Not only developers and managers of companies, but also ordinary users and employees, who will use the technologies themselves and recommend their use in companies, should talk about potential opportunities. We need large-scale, spectacular, viral cases like PokemonGo.

Table 5

SWOT analysis of the use of augmented and virtual reality technologies

|

Strengths: |

Weaknesses: |

|---|---|

|

• diversity of applications; |

• technological limitations and software imperfections; |

|

• active management; |

• lack of quality content; |

|

• innovativeness; |

• high costs; |

|

• powerful 3D tool; |

• lack of qualified personnel; |

|

• real-time interaction |

• negative health effects |

|

Capabilities: |

Threats: |

|

• high market potential, availability of free niches; |

• competitive technologies (Internet of things, artificial intelligence, robotics); |

|

• readiness of the environment (companies) to implement the technology; |

• lack of information on the results of use; |

|

• growing interest of investors; |

• unpredictability of external environment; |

|

• development of adjacent markets |

• young market |

Using the potential of these technologies companies will be able to achieve an increase in profits due to the growth of employee productivity, optimizing work and production processes, attracting new customers and deepening professional competencies of their employees.

The analysis of capabilities and weaknesses of the augmented and virtual reality technologies, the main problems that businesses may encounter at the stage of their implementation and subsequent operation, makes it possible to determine a number of factors of the external and internal environment. Knowing them, Russian companies will be able to minimize the negative consequences of using these technologies:

Regulations were adopted [Regulation, 2017; Decree, 2017; Decree 2018] aimed at the development of information society, formation, support and regulation of the national digital economy, ensuring the global competitiveness of the Russian science as well as support for domestic software developers.

One of the key areas for the development of digital environment is assistance to the development of the existing and creation of new conditions for the emergence of breakthrough and promising end-to-end digital platforms and technologies, including the technologies of augmented and virtual reality. In particular, by the end of 2018 it is planned to determine a list of the necessary standards and resources in the field of information security adopting the relevant national standards by mid-2020 [Order, 2017]. These measures will reduce the risks associated with information security of augmented and virtual reality.

In developing national projects in the field of education, science and digital economy the focus should be on the following tasks:

One should note the activities of the National Technology Initiative, in particular, the plan of activities ("road map") "NeuroNet". According to this document, by 2025 it is planned to implement a number of activities to integrate the virtual and augmented reality systems in education, medicine, entertainment and sports; by 2035 the implementation of human integration with the virtual environment is expected.

Therefore, the state plans to provide comprehensive support to developers in the field of technologies of augmented and virtual reality.

The development of technologies is facilitated by the creation of specialized communities (the Association of Augmented and Virtual Reality, “VR Consortium”, the industrial union “NeuroNet”) uniting representatives of business, government and individuals working in the industry. The joint efforts help identify the main potential directions of development, provide comprehensive support in the development and monetization of these technologies. International educational activities are conducted, which is an essential aspect of successful development of technologies in B2C sector in the near future.

The global market of virtual reality technologies is in the formative stage, the international division of competences is not yet complete, the main global content producers are not taking significant actions yet. In the devices segments the leading technological companies have been established, but the Russian content and software developers have every chance to take a worthy position among foreign competitors and become suppliers of technological and VR solutions in the field of virtual reality (especially for Asian countries).

The rapid development of the national animation industry in the last 5 years has led to the emergence on the market of numerous highly skilled animators, artists, computer graphics visualization experts. In addition, a strong school of programmers and engineers has developed in Russia.

Under the favorable conditions of the foreign exchange market and the ruble exchange rate against world currencies, the highly skilled work of Russian developers in the field of content and software has become extremely competitive regarding the global price for the work of similar quality. Their skills may be in demand primarily in the areas of animation, children's and educational applications, project visualization in virtual reality.

In this study we have analyzed the possibilities of use of the virtual and augmented reality technologies in business processes of companies identifying the main factors hindering the implementation of these technologies in Russian companies.

1. Autonomous non-commercial organization Sochi 2014 Olympic and Paralympic Winter Games Organizing Committee// NextSpace.URL: https://next.space/portfolio/sochi-2014/.

2. Revizto team blog. User Experience// Revizto. URL: https://revizto.com/ru/blog/cases.

3. Interactive museum for children "My future profession"// ARProduction. URL: http://arproduction.ru/cases/museum/.

4. Lvov M. (2016) Virtual reality becomes real // Mediavision. URL. http://mediavision-mag.ru/uploads/08-2016/48_49_Mediavision_08_2016.pdf.

5. In 2018 the global AR / VR market will grow to $ 18 billion (2017) // Computerworld Russia. № 19. URL: https://www.osp.ru/cw/2017/19/13053468/.

6. Order of the Government of the Russian Federation of 28.07.2017 N 1632-p “On approval of the program “Digital Economy of the Russian Federation” // Consultant Plus.

7. URL: http://www.consultant.ru/document/cons_doc_LAW_221756/.

8. The market of virtual reality in Russia ([2017]) // Institute of Modern Media (MOMRI). URL: http://momri.org/wp-content/uploads/2017/04/MOMRI.-VR-market-in-Russia.-April-2017-rus.pdf.

9. Trachuk A.V., Linder N.V. (2016) Adaptation of Russian firms to changes in the external environment: the role of e-business tools // Management №1. P. 61–73.

10. Trachuk A.V., Linder N.V. (2017a) Innovations and productivity of Russian industrial companies // Innovations. № 4 (222). P. 53–65.

11. Trachuk A.V., Linder N.V. (2017b) Innovations and productivity: empirical study of the factors preventing growth by using the method of longitudinal analysis // Management Sciences. Vol. 7, № 3. P. 43–58.

12. Trachuk A.V., Linder N.V. (2017c) The prospects for the use of mobile payment services in Russia: theoretical approach to understanding the factors of distribution // Bulletin of the Faculty of Management of Saint-Petersburg State University of Economics. № 1-1. P. 322–328.

13. Trachuk A.V., Linder N.V. (2017) Distribution of e-business tools in Russia: the results of empirical research // The Russian Journal of Management. Vol. 15, № 1. P. 27–50.

14. Presidential Decree of 09.05.2017 N 203 “On the Strategy of development of information society in the Russian Federation in 2017–2030” // Consultant Plus. URL:http://www.consultant.ru/document/cons_doc_LAW_216363/.

15. Presidential Decree of 07.05.2018 N 204 "On the national goals and strategic objectives of development of the Russian Federation for the period up to 2024" // ConsultantPlus. URL: http://www.consultant.ru/document/cons_doc_LAW_297432/.

16. Digital decade. In tune with the times (2017) // PWC. URL: https://www.pwc.ru/ru/publications/global-digital-iq-survey-rus.pdf.

17. After mixed year, mobile AR to drive $108 billion VR/AR market by 2021 (2017) // Digi-capital. URL: https://www.digi-capital.com/news/2017/01/after-mixed-year-mobile-ar-to-drive-108-billion-vrar-market-by-2021/.

18. 2018 Augmented and Virtual Reality Survey Report (2018) // Perkins Coie and Upload. URL: https://www.perkinscoie.com/images/content/1/8/v2/187785/2018-VR-AR-Survey-Digital.pdf.

19. Augmented Reality and Virtual Reality Market by Offering (Hardware & Software), Device Type (HMD, HUD, Handheld Device, Gesture Tracking), Application (Enterprise, Consumer, Commercial, Healthcare, Automotive), and Geography — Global Forecast to 2023 (2018) // Markets and Markets. URL: https://www.marketsandmarkets.com/Market-Reports/augmented-reality-virtual-reality-market-1185.html.

20. Azuma R. T. (1997) A Survey of Augmented Reality // Presence: Teleoperators and Virtual Environments. Vol. 6, N 4. P. 355–385.

21. Caudell T. P., Mizell D. W. (1992) Augmented reality: an application of heads-up display technology to manual manufacturing processes // Proceedings of the Twenty-Fifth Hawaii International Conference on System Sciences. 7-10 Jan. 1992. URL: https://ieeexplore.ieee.org/document/183317/.

22. 5 Conclusions From John Riccitiello VRLA 2017 Keynote on VR (2017) // AppReal. URL: https://appreal-vr.com/blog/5-conclusions-from-john-riccitiello-vrla-2017-keynote-on-vr/.

23. Future Reality: Virtual, Augmented & Mixed Reality (VR, AR & MR) Primer (2016) // Bank of America Merryll Lynch. URL: https://www.bofaml.com/content/dam/boamlimages/documents/articles/ID16_1099/virtual_reality_primer_short.pdf.

24. Heilig M. L. (1992) El Cine delFuturo: The Cinema of the Future // Presence: Teleoperators and Virtual Environments. Vol. 1, N 3. P. 279–294.

25. Kaiser R., Schatsky D. (2017) For more companies, new ways of seeing. Momentum is building for augmented and virtual reality in the enterprise // Deloitte University Press. URL:https://www2.deloitte.com/content/dam/insights/us/articles/3768_Signals-for-Strategists_Apr2017/DUP_Signals-for-Strategists_Apr-2017.pdf.

26. Krueger M.W. (1983) Artificial Reality. NewYork: Addison-Wesley.

27. Kunkel N., Soechtig S., Miniman J. et al. (2016) Tech Trends 2016: Augmented and virtual reality go to work. [S.l.]; Deloitte University Press // Deloitte University Press. URL: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Technology/gx-tech-trends-2016-innovating-digital-era.pdf.

28. LaValle S. M. (2017) Virtual Reality / University of Illinois. [S.l.:] Cambridge University Press. 418 p. URL: http://vr.cs.uiuc.edu/vrbook.pdf.

29. Milgram P., Kishino F. (1994) A taxonomy of mixed reality visual displays // IEICE Transactions on Information and Systems. Vol E77-D, N 12. P. 1321–1329.

30. OPS Solutions to Display the Power of Enterprise AR at HANNOVER MESSE 2018 (2018) // Light Guide Systems. URL: http://lightguidesys.com/blog/ops-solutions-display-power-enterprise-ar-hannover-messe-2018/.

31. Panetta K. (2017) Top Trends in the Gartner Hype Cycle for Emerging Technologies // Gartner. URL: https://www.gartner.com/smarterwithgartner/top-trends-in-the-gartner-hype-cycle-for-emerging-technologies-2017/.

32. Profiles in Innovation: Virtual & augmented reality. Understanding the race for the next computing platform (2016) // Goldman Sachs. URL: http://www.goldmansachs.com/our-thinking/pages/technology-driving-innovation-folder/virtual-and-augmented-reality/report.pdf.

33. Sutherland I. E.(1965) The Ultimate Display // Proceedings of IFIP 65. Vol. 2. URL: http://worrydream.com/refs/Sutherland%20-%20The%20Ultimate%20Display.pdf.

34. Trachuk A., Linder N. (2017) The adoption of mobile payment services by consumers: an empirical analysis results // Business and Economic Horizons. 2017. Vol. 13, N 3. P. 383–408.

35. Vince J. (1995) Virtual reality systems. New York: ACM Press; Addison-Wesley Publishing Co. 388 p.

36.

Chief expert of Division of the budgetary policy in the sphere of justice, the prevention and elimination of consequences of emergency situations of Department of the budgetary policy in the sphere of military and law-enforcement service and the state defense order of the Ministry of Finance of the Russian Federation. Research interests: new technologies, distribution of innovations, technological business, modern business-models.

Ivanova A.V. VR & AR TECHNOLOGIES: OPPORTUNITIES AND APPLICATION OBSTACLES. Strategic decisions and risk management. 2018;(3):88-107. https://doi.org/10.17747/2078-8886-2018-3-88-107

Ligovsky av 73, of.401, Saint Petersburg, 190040, Russia

Tel.: +7 (812) 346-50-15 (16)

Real Economy Publishing House.

E-mail: info@jsdrm.ru

Registration certificate PI No. FS-77 - 72389 from 02.28.2018, issued by the Federal Service for Supervision in the Sphere of Communications, Information Technologies and Mass Communications.

Processing of personal data